M&A in Türkiye continues to perform

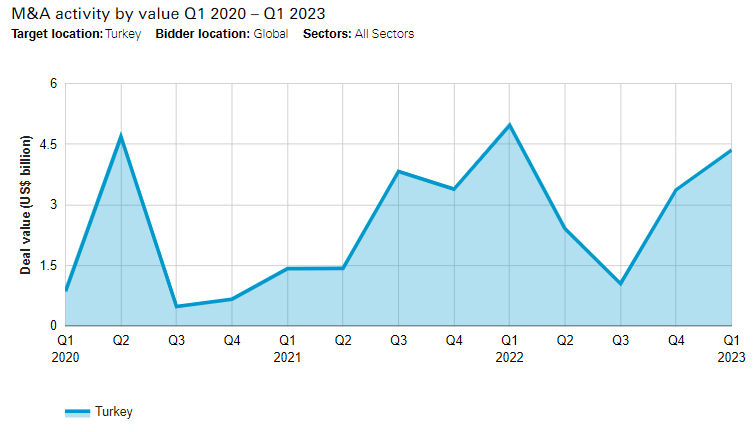

M&A activity in Türkiye bucked global trends in 2022, posting more deal value than in 2021. Meanwhile, activity in the rest of the world dipped as geopolitical and inflation concerns curbed acquirers’ appetite. Transaction value totaled US$11.8 billion in Türkiye last year, a gain of more than 17% year-on-year. The first quarter of 2023 continued this upward trend reaching US$4.4 billion, up almost 30% on the previous quarter.

And while deal volume was not as enthusiastic last year—the tally fell by 24% year-on-year in 2022 to 126 transactions—Q1 2023 has seen a 17% quarterly increase and remains above pre-pandemic levels with 28 deals. It’s anticipated that M&A in Turkey may improve during the second half of 2023 as a result of political and socio-economic stability post elections.

There was a clear trend toward domestic activity in Q1 2023. More than 94% of all deal value and nine of the top-ten deals were attributable to Turkish parties on the buy side, according to Mergermarket.

The buoyancy of corporate M&A is not mirrored in the private equity (PE) market, which dropped significantly since mid-2022. Inflation has been a major concern in Türkiye for some time, with the country’s consumer price index surging to nearly 86% on an annual basis in October 2022. That has since cooled off sharply but remained at nearly 44% as of April. As a result, international PE funds, which must manage their currency risk in the face of the devaluing lira and which lack the same strategic imperatives as corporate acquirers, appear to be biding their time for now.

In Q1 2022, there were six PE deals worth a combined US$1 billion. But in Q4 2022, not a single deal was recorded. In Q1 2023, only one deal was struck.

Domestic firms such as Turkven and Actera continue to raise fresh pools of capital from investors, the former having already held an interim close on its Turkey Growth Fund IV. Near-term sponsor-led activity centered on the mid-market (and mainly on sectors like tech, gaming, financial solutions, etc.) is likely, as well as growth and venture capital deals since they do not rely on debt financing.

Sectors play a big part

Activity in the country continues to be sector driven and given the size of the market, larger deals can skew annual deal value totals quite heavily. For example, the Türkiye Wealth Fund (TWF)—the national sovereign wealth fund launched in 2016 to develop the country’s most strategic assets—made capital injections into two banks in Q1 2023 to help shore up lending in the economy. State-owned VakıfBank and Halkbank were given US$1.7 billion and US$1.6 billion investments, respectively, in exchange for stakes of 33% and 35%. The two deals pushed Türkiye’s financial services sector to the top of the value leaderboard in the quarter, with deals totaling US$3.3 billion.

It was a similar story in 2022, when the technology, media and telecommunications sector dominated, with US$5.2 billion of aggregate transacted value, a 44% share of total deal value for the year and vastly outpacing any other sector. More than half of this came from a single play—the acquisition of a 55% stake in the country’s largest telco, Türk Telekom, by TWF, representing a deal value of US$3.2 billion. The investment is expected to support Türk Telekom’s technology innovation.

The energy, mining and utilities sector also saw fairly brisk deal activity in the past 12 months. Deals in the sector totaled just under US$3 billion in 2022, some way behind TMT but leading on volume with 24 deals—a 19% share across all sectors. When Abu Dhabi conglomerate International Holding Company (IHC) acquired a 50% stake in Turkish Kalyon Energy through one of its subsidiaries, the deal was singled out as the largest energy sector transaction in 2022. While Q1 deals in the sector were down—with just one deal valued at US$53 million—there is good reason to assume more could appear in the months ahead, specifically in the renewables realm. As an EU member, Türkiye is committed to meeting its clean energy targets and, as of 2022, approximately 54% of electric power generation capacity came from sources such as hydroelectric, wind, solar, geothermal, and biomass power plants, according to the International Trade Administration, making the country the fifth largest generator of renewable energy in Europe and the twelfth largest in the world. The government is working to address bottlenecks, with investments into new transmission and distribution infrastructure required to accommodate the growing volume of renewable electricity produced in the country.

Outlook remains positive

The elections in May 2023 saw the incumbent president Recep Tayyip Erdoğan retain power, while the president’s parliamentary bloc also won a majority of seats in the parliamentary race. The prevailing view in Istanbul is that post re-election, the administration could begin to change tack due to the pressures felt throughout the election period, as opposition support grew.

In any case, greater political certainty should lay the foundations for continued corporate M&A, as strategic Gulf investors show unwavering interest in Türkiye’s energy sector and sovereign capital remains committed to deals.

Foreign investment is likely to continue and improve in certain sectors. In addition to ongoing energy sector investment, we will continue to see new investments into companies operating in the tech, gaming and financial solutions sectors, as well as FMCG companies.

Türkiye and the UAE have been working to strengthen their diplomatic and economic ties. This was recently evident in the latter providing the most relief aid to Türkiye among the Gulf Cooperation Council members in the wake of the earthquake, providing search and rescue teams, field hospitals, supplies, and financial assistance to the Turkish government. This coincided with both sides further mending relations with the signing of a historic free trade deal in February 2023, with the aim of more than tripling mutual trade volume to US$25 billion over the next five years.

Judging by the first months of 2023, this year is on course to deliver yet again despite the residual macro challenges the country faces.